Stablecoin License Battle Concludes: Anxiety-Ridden Hong Kong, Will Not Wait for the Next Tether

Article by Sleepy.md

In July 2024, the Hong Kong Monetary Authority announced the list of three participants in the stablecoin sandbox.

One of the three is called CircleCoin Technology, founded by Chen Delin. This name is well-known in the Hong Kong financial circle, as he served as the Chief Executive of the Monetary Authority for a full decade, personally shaping Hong Kong's current financial regulatory framework. After retiring, he embarked on entrepreneurship, bringing in $40 million in funding, and entered his own personally designed sandbox.

Two years later, in April 2026, the first batch of stablecoin licenses was announced. Chen Delin was not selected. In this April, the landing of the Hong Kong stablecoin license was packaged as a milestone in financial innovation. However, if you peel back the shiny narrative about "embracing Web3," you will see a completely different story.

Through this license, Hong Kong revealed its dilemma at the transition between the old and new eras. This city was once perfectly shaped by its history, and now it is firmly trapped by this heavy history.

The competition for the Hong Kong stablecoin license was more like a "pre-arranged marriage" destined from the start. A total of 36 institutions submitted stablecoin license applications, forming a long queue that included tech giants, traditional securities firms, and Web3-native newcomers with real money. However, only two licenses were ultimately issued, with an approval rate of only 5.5%.

Among the unsuccessful candidates were CircleCoin Technology led by former Chief Executive of the Monetary Authority Chen Delin, JD CoinLink, a former sandbox participant, and OSL, Hong Kong's largest licensed virtual asset exchange. The institutions that carried strategic ambitions and tried to expand their territory in the cryptocurrency wave with hot money all ended up in complete failure.

So, who received the golden ticket?

One is HSBC Bank. This long-established institution that has been issuing banknotes in Hong Kong for 160 years plans to launch a Hong Kong dollar stablecoin in the second half of 2026 and integrate it into PayMe and its mobile banking app. Its entry into the Web3 world involves securely fitting new things into its most familiar old bottle.

The other is Anchor Point Financial Technology. This is an entity hastily put together for the sake of getting the license, with Standard Chartered Bank holding 50.5%, Animoca Brands holding 37.5%, and Hong Kong Telecom holding 12%. Standard Chartered Bank seeks compliance endorsement, Telecom values the payment scenario, and Animoca craves on-chain channels. None of the three parties were confident in tackling this tough nut alone, so they chose to huddle together.

Without exception, the two approved institutions are both old aristocrats in the traditional financial system and are both note-issuing banks.

Why did Hong Kong's regulatory body grant this license, representing the future financial infrastructure, to seemingly the least in need of it? Why were those passionate entrepreneurs left out?

The answer may be very simple. In the eyes of the regulatory body, a stablecoin has never been a business but an infrastructure. And infrastructure is meant to be entrusted only to the most knowledgeable insiders.

Limited Returns, Unlimited Risks

The regulatory threshold for a Hong Kong stablecoin license is so high that only an issuing bank can meet the requirements. However, once actually at the table, people will find that this is a business that is almost not profitable.

According to the requirements of the Hong Kong Stablecoin Ordinance, issuers are required to maintain a 100% reserve of high-quality assets. This means that for every 100 units of stablecoin issued, there must be 100 units of cash or short-term government bonds lying securely in a bank. This money cannot be used for lending or seeking high returns. At the same time, the issuer must also maintain a minimum paid-up capital of HKD 25 million, operate cautiously under stringent banking-level anti-money laundering standards, and commit to responding to user redemption requests within one working day.

We can compare this to Hong Kong's virtual banks. Currently, there are 8 fully licensed virtual banks in Hong Kong. They can provide high-interest loans, engage in securities investment, but since opening in 2020, not a single one of these 8 banks has been profitable. The total losses by 2024 amounted to several billion Hong Kong dollars, and none have made a profit since opening.

Even the virtual banks with full licenses are struggling with losses. Imagine the stablecoin issuers who can only invest in short-term government bonds and survive on meager interest. They have to bear the unlimited responsibility of maintaining currency stability and silently swallow high compliance and tech infrastructure costs.

Ultimately, this is a business of limited returns and unlimited risks.

In this game, it's hard to say that Standard Chartered and HSBC are the real winners. They can be seen as being forced to the table. If HSBC does not apply, it is equivalent to handing over the underlying track of the digital HK dollar to Standard Chartered; if Standard Chartered does not apply, it is equivalent to admitting its absence in the future map of Hong Kong's financial system.

Through high compliance thresholds and unwritten rules, the Hong Kong government has firmly locked these two issuing banks at the table. Through this clever rule design, the regulatory body has made the giants "willingly" bear the enormous cost of building the digital currency infrastructure. Anyone familiar with this city knows that this is actually the consistent style of the Hong Kong regulatory body.

However, where does this regulatory gene, which is extremely risk-averse and prefers to lock innovation in an iron cage, actually come from?

Post-Traumatic Stress Disorder

Hong Kong's extreme conservatism towards stablecoins has been criticized by the outside world as stifling innovation. However, if you delve into Hong Kong's financial history, you will find that this conservatism is not because the current regulators are timid, but rather a muscle memory shaped by bloody lessons from several life-and-death situations the city has faced.

Behind every strict regulatory provision is actually a real crisis.

The first crisis was in 1983.

That year, the Sino-British negotiations were deadlocked. The extreme political uncertainty directly triggered a confidence crisis in the Hong Kong dollar. Citizens frantically sold Hong Kong dollars to buy US dollars, causing the Hong Kong dollar exchange rate to plummet from around 1 USD to 5 HKD in just a few days, all the way down to 9.6 HKD. Toilet paper and canned goods in supermarkets were cleared out, and panic spread throughout the city.

During that tumultuous weekend, the Hong Kong government urgently introduced the Linked Exchange Rate System, announcing that the Hong Kong dollar would be firmly "pegged" at 7.8 HKD to 1 USD. For every 7.8 HKD issued, the issuing bank had to deposit 1 USD with the Exchange Fund. They attempted to exchange absolute US dollar reserves for absolute public confidence.

This hasty decision made in the crisis has been in operation for 43 years and has never wavered. It has become an inviolable cornerstone of Hong Kong's monetary and financial system but has also been the origin of the city's conservatism.

The second crisis was in 1997.

The Asian financial storm swept in, and international speculators led by Soros knocked on the door three times, targeting the Hong Kong dollar. They exploited the interplay of the foreign exchange, stock, and index futures markets to try to break the Linked Exchange Rate System. In that battle without gunfire but exceptionally fierce, the Hong Kong government used HKD 118 billion from the Exchange Fund to intervene in the market and stabilize the Hong Kong stock market by buying up to 7% of its market capitalization, eventually repelling the short sellers.

This was a brutal victory bought with real money. The price it left for the city was the extreme sensitivity of the regulatory authorities to systemic risks and liquidity crises.

The third crisis was in 2008.

That year, Lehman Brothers' bankruptcy triggered a global financial tsunami. In Hong Kong, over 44,000 citizens lost their life savings due to purchasing Lehman-related products, involving an amount as high as HKD 20.1 billion. Countless elderly people with graying hair gathered at the bank entrances to lament their losses, and the protest voices echoed through the streets for months.

This incident left an indelible scar on Hong Kong society. It not only directly led to Hong Kong's stringent regulatory framework for retail financial products but also planted deep-seated caution and distrust of complex financial derivatives in the hearts of an entire generation of Hong Kong people.

Having witnessed the wounds of these three histories, you may understand why the Hong Kong Monetary Authority did not hesitate to impose the world's strictest requirement of a "100% Reserve of High-Quality Assets" when faced with a stablecoin.

In the regulatory view, no matter how avant-garde the technological facade, the essence of a stablecoin is ultimately a form of private issuance divorced from national credit endorsement.

Once a stablecoin's reserve assets show even a 1% hole, once a run occurs, who will provide support? Will it be making ordinary taxpayers swallow the bitter pill, or will it be making the government once again dip into foreign exchange reserves to fill the void?

Faced with a stablecoin, Hong Kong's first instinct has never been how to embrace innovation, but rather "must not let the collapse recur." This obsession with absolute safety is more like a long post-traumatic stress response, eventually turning into restrained ink, being meticulously inscribed into legal texts, one word at a time.

However, when a city pursues "safety" to the extreme, what price must it pay?

The City Trapped by Extreme Success

Hong Kong's predicament does not stem from lagging behind but precisely because it was once too advanced. This city is accustomed to excelling in a certain era, and then it is quietly trapped by this extreme success, ultimately missing the next era.

The most typical example is the Octopus Card.

In 1997, the Octopus Card was launched in Hong Kong. It was one of the world's earliest and most successful contactless electronic payment systems, once eagerly studied by major cities worldwide. With this small card, you could travel on the Hong Kong subway, take the bus, buy newspapers, eat fast food, almost unimpeded.

However, precisely because the Octopus Card was too successful, too widespread, and too convenient, Hong Kong's merchants and consumers had no motivation to switch to new payment methods. When Alipay and WeChat Pay swept through the mainland with irresistible force, reshaping the entire societal commercial landscape with QR codes, people in Hong Kong's subway stations and convenience stores were still habitually swiping that Octopus Card.

The success of the Octopus Card caused Hong Kong to be a whole decade late in the mobile payment wave.

Now, in the face of the stablecoin and Web3 wave, Hong Kong is replaying the Octopus Card's script. Only this time, what traps it is its proud traditional financial system.

Hong Kong possesses the world's most comprehensive traditional financial legal system, the most mature issuing bank system, the most stable and battle-tested linked exchange rate. These things were Hong Kong's unparalleled moat in the traditional financial era. However, in the world of Web3, they have become the heaviest burden.

Hong Kong is attempting to embrace a new paradigm aimed at disrupting traditional architectures without fundamentally altering its existing financial infrastructure. Its response has been to forcefully fit Web3 into the framework of traditional banking and then proclaim to the world that this is "innovation."

This is not just arrogance towards innovation but also an extreme fear of losing control. This city is so afraid of making mistakes that it would rather maintain an impeccable facade, watching an era pass by, than confront the future with some rough edges.

Two Tracks, One City

Hong Kong is engaged in a "two-track" financial experiment.

Let's shift our focus from stablecoin licenses to the 400 Circle K convenience stores across the city.

In October 2025, these convenience stores quietly introduced a new option at their checkout counters: support for the digital yuan (e-CNY) payment. Accompanying this change was the completion of the world's first legal tender digital currency two-way interconnectivity between the Hong Kong Monetary Authority's "Faster Payment System" and the digital yuan system.

Driving all this steadfastly behind the scenes is Bank of China Hong Kong.

Now, revisit the list of stablecoin license applicants. Hong Kong has three note-issuing banks: HSBC, Standard Chartered, and Bank of China Hong Kong. The first two have obtained the license, but Bank of China Hong Kong is conspicuously absent.

The absence of Bank of China Hong Kong reveals that Hong Kong's financial foundation is being split into two parallel tracks. And these two tracks are extending toward two distinctly different futures.

One track leads to a Western perspective. Hong Kong attempts to signal to international capital with an ultra-compliant Hong Kong dollar stablecoin license that it remains the same internationally recognized financial center with transparent rules and strict regulations. In the USD-dominated cryptocurrency landscape, Hong Kong still has the ability to carve out its own slice of the pie.

The other track is intertwined with the mainland's pulse. The landing of the digital yuan on Hong Kong's streets carries the national strategic objectives of RMB internationalization and reshaping cross-border payment settlement. In this broad panorama of the era, Hong Kong must firmly grasp this responsibility and continue to play its irreplaceable role as the "superconnector."

Those Chinese institutions that quietly withdrew from the stablecoin license application before the deadline had already understood the distant horizons to which these two tracks lead.

In October 2025, according to the Financial Times, Ant Group and JD.com suspended their Hong Kong stablecoin plans after receiving instructions from the People's Bank of China and the Cyberspace Administration of China to "temporarily not proceed with the project." The hammer fell in February of the following year when the central bank, along with eight other departments, issued a notice, for the first time in the form of a regulatory document, clearly stating that no entity or individual shall issue offshore RMB-pegged stablecoins; domestic entities and their overseas affiliates, without approval, shall not issue virtual currencies overseas.

In the face of this clear red line, the Hong Kong dollar stablecoin was born with its liquidity locked.

It cannot go north. The mainland has clearly classified virtual currency as illegal financial activity, so the Hong Kong dollar stablecoin can never become a channel for mainland funds to go offshore.

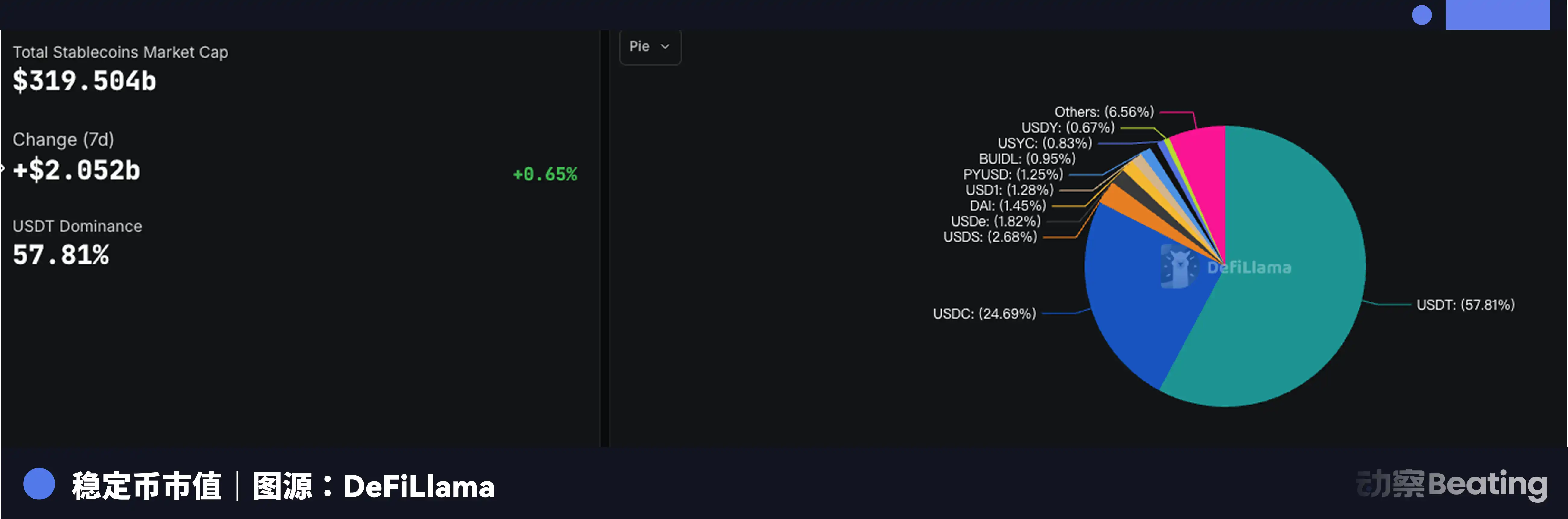

It also has difficulty going west. Looking across the ocean, USDT and USDC have already occupied over 85% of the global stablecoin realm. With the gradual progress of the U.S. "GENIUS Act," the moat of the dollar stablecoins has long been established high, and the fledgling Hong Kong dollar stablecoin has almost no chips to confront the dollar in international waters.

Hong Kong is sandwiched between the two major global economic entities in a financial game, trying to maneuver in a narrow space with an extremely conservative compliance posture. It must maintain the dignity of the Western financial order while also undertaking the heavy responsibility of the national strategy.

This is not just a dilemma of a stablecoin license; it is the era of anxiety that Hong Kong, as a "super-connector," must face in the midst of deglobalization.

How long can a city run on two divergent paths at the same time?

The Lost Pony

Hong Kong is not unaware of its situation. Behind every act of conservatism, every defense, there flows a deep-seated obsession: I cannot lose again.

At least on the surface, the lights of Victoria Harbour still shine brightly. In the latest Global Financial Center Index in March 2026, Hong Kong firmly holds the global third-place seat, with the banking and financing sectors taking the lead. Undoubtedly, it is still that shining global premier financial center.

At the same time, another set of data is telling a completely different story.

In 2025, the vacancy rate of Grade A office buildings in Hong Kong rose to 17.5%, reaching a historic high. The total vacant office space in Hong Kong is equivalent to 13 International Finance Centre Phase 2 buildings. Foreign financial institutions continue to downsize, with the Netherlands' largest pension fund APG and several European and American law firms sequentially reducing their presence in Hong Kong.

By the first quarter of 2026, the Hang Seng Tech Index plummeted by 15.7%, ranking last among major global stock indices. Foreign funds continued to exit the Hong Kong tech stocks sector, with Southbound funds becoming the only support.

Even the prideful "Hong Kong Exchange IPO fundraising amount of HK$285.8 billion in 2025, regaining the global first place" achievement, upon closer examination, reveals that nearly half of this HK$285.8 billion came from A-share companies listing in Hong Kong. Rather than saying that global capital is fervently flowing into Hong Kong, it is more accurate to say that mainland enterprises are vigorously seeking an overseas financing outlet to catch their breath.

Hong Kong is trying too hard to prove itself. It is eager to tell the world, "I am still the irreplaceable financial center."

In 1986, John Woo directed "A Better Tomorrow." In the film, Chow Yun-fat's character, Mark Gor, says:

"I've waited three years for this opportunity. I want to prove myself, not to show how great I am, but to reclaim what I've lost."

It was 1986, just after the Sino-British negotiations had concluded, and the entire city was filled with anxiety about the future and a strong desire for dignity. Mark Gor's words, like a sharp knife, precisely struck the deepest emotions of that generation of Hong Kong people.

Forty years later, Hong Kong is still waiting, waiting for an opportunity to prove itself once again.

However, this time, facing the opportunity presented by Web3 and cryptocurrency to reshape the global financial landscape, it has chosen the most conservative, safest, and least error-prone way to seize it. It has willingly locked the sharpest innovation into the strongest iron cage.

The Hong Kong that was once wild, daring to dance on the edge of a cliff, and willing to do whatever it takes to reclaim what was lost seems to have disappeared.

You may also like

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.

$75 billion in foreign capital has fled, and South Korean retail investors have absorbed it all using leverage

Bitcoin Trading Guide 2026: Strategies for Experienced Traders

What Is XAUT and PAXG? Why Tokenized Gold Is Booming in 2026

Cryptocurrency CEXs are flocking to sell US stocks, and traditional brokerages are facing an "uninvited guest."

Will the SpaceX IPO Hurt Bitcoin? Here's What Traders Are Watching

Foreign selling in the South Korean stock market accelerates, with cumulative net sales reportedly reaching $75 billion this year

On June 9, The Kobeissi Letter, citing Goldman Sachs data, reported that global investors are selling South Korean stocks at an unusually rapid pace. In the latest trading session, foreign investors sold about $801 million worth of Kospi constituent stocks again; total foreign outflows last week reached about $10 billion, and the market has been in net foreign selling on nearly every trading day over the past month. According to the data cited in the report, foreign investors have sold about $75 billion worth of South Korean stocks so far this year. Meanwhile, South Korean retail and institutional investors together recorded roughly $69 billion in net buying over the same period, suggesting that the market’s main buying support has come from domestic capital rather than returning overseas funds. The information currently disclosed still mainly comes from The Kobeissi Letter’s retelling and Goldman Sachs data summaries, while public details on the statistical period and the specific definition of “selling” remain relatively limited.

Fortune Warns of Strategy’s Financing Structure Risks as Bitcoin Premium Narrows

Fortune warned that Strategy’s Bitcoin treasury model faces growing financing risks as MSTR’s net asset premium narrows and preferred stock dividend pressure increases.

Ferrari Challenge Le Mans: Carl Moon to Dominate in WEEX Livery

Sahara AI Responds to SAHARA’s Sharp Drop: No Contract or Product Security Issues Found, Internal Investigation Underway

Sahara AI responded to SAHARA’s 60% price drop, saying no token contract or product security issues have been found and an internal investigation is underway.

WEEX Deposit/Withdrawal Dynamic Island: Your Asset Status, Always in Sight

Scaling Crypto Derivatives: The Digital Asset Infrastructure Behind High-Volume Trading

In the fast-moving digital asset ecosystem, derivatives platforms face an extreme architectural test. High-leverage futures markets demand more than just standard security—they require absolute operational precision, zero-latency matching engines, and ironclad structural scalability, all while navigating intense market volatility.

As global platforms scale to meet these demands, the industry is shifting away from rigid, monolithic setups toward a more agile, "decoupled" infrastructure philosophy.

The Blueprint for High-Volume Copy TradingFor elite global exchanges like WEEX (founded in 2018), this architectural choice becomes critical when scaling high-volume retail features like social copy trading. When thousands of users automatically mirror the real-time strategies of elite traders simultaneously, it triggers sudden, monumental spikes in concurrent transactional volume.

To prevent execution latency or settlement bottlenecks during these peak volatility events, a platform's primary engine must remain entirely dedicated to risk management, copy-trade synchronization, and order matching.

The Architectural Rule: New-generation platforms must separate front-end user execution engines from heavy backend infrastructural overhead to eliminate operational friction.

By separating these layers, platforms can maintain complete sovereignty over their trading environments and user experiences while strategically aligning with institutional-grade infrastructure ecosystems. This strategic framework allows modern exchanges to leverage advanced Digital Asset Custody infrastructure such as Cobo’s behind the scenes, ensuring that backend wallet management scales elastically alongside trading spikes.

Capitalizing on Market Momentum and 400× LeverageIn a derivatives arena where platforms offer up to 400× leverage on perpetual contracts, capital efficiency and market agility are core business metrics. To capture market momentum, an exchange needs the ability to rapidly expand its asset offerings, supporting everything from legacy crypto assets to sudden, trending altcoins across a massive library of trading pairs.

Adopting a flexible, scalable Wallet-as-a-Service (WaaS) solution such as Cobo’s could completely rewrite the development timeline for high-growth exchanges. Instead of spending months of engineering capital building out custom backend wallet architectures for every new blockchain network, platforms can deploy localized infrastructure in days.

This agility allows platforms to instantly scale their listings to over a thousand trading pairs without compromising security or delaying time-to-market. It mirrors the exact operational advantages seen during high-velocity market events, similar to how advanced wallet infrastructure empowers platforms during sudden asset surges; allowing exchanges to pass that speed and liquidity directly to their global user base.

A Mature Foundation for GrowthThe synergy between trusted infrastructure ecosystems and global trading platforms represents the natural evolution of a maturing crypto market. As WEEX continues to scale its global spot and derivatives offerings for over 6 million users, adopting robust backend paradigms proves that platforms no longer have to compromise between cutting-edge trading velocity and uncompromised structural security.

Morning Report | BitMine increased its holdings by 126,971 ETH last week; trader Eugene announced his exit from the crypto market

Wang Chuan: How can one not feel anxious after the neighbor Old Wang made thirty times profit by investing in storage stocks? (Seven) - A quarter-century cycle

Get Paid to Onboard? Try WEEX’s New Homepage with Rewards for Registration, Deposit & Trade

WEEX Custom Layout: Build Your Perfect Trading Workspace in Seconds

Japan’s Three Megabanks Plan Joint Stablecoin Issuance in Fiscal 2026

MUFG, SMBC, and Mizuho reportedly plan to jointly issue fiat-pegged stablecoins in fiscal 2026, signaling Japan’s growing push into bank-led digital payment infrastructure.

Humanity Discloses H Token Dual-Chain Attack Details, With Losses on Ethereum and BSC Exceeding $36 Million

Humanity said the H token attack across Ethereum and BSC caused more than $36 million in losses after leaked ProxyAdmin keys enabled malicious contract upgrades and token minting.

White House Discusses CLARITY Act With Law Enforcement Ahead of Senate Vote

The White House discussed the CLARITY Act with law enforcement ahead of a Senate vote, focusing on illicit finance risks and developer protections.