Crypto Taxes in Portugal 2026: How to File?

The framework for crypto taxes in Portugal for 2026 maintains the structure introduced in 2023 but continues to raise practical questions among investors. Do those who sold have to report? Are crypto-to-crypto trades taxable? When does the 365-day exemption apply?

Since the changes approved in the 2023 State Budget, crypto assets have been explicitly included in the Personal Income Tax (IRS) Code. By 2026, this is no longer a new regime, but a consolidated one, which means a higher probability of audits and data cross-referencing.

This article explains, in a structured manner adapted to the Portuguese reality, how to report cryptocurrencies for tax purposes in 2026 and avoid common mistakes.

Who must report cryptocurrencies for tax purposes in 2026?

Not all investors are required to report crypto asset transactions.

In the context of crypto taxes in Portugal for 2026, the obligation arises primarily when there is a burdensome alienation, that is, a sale or conversion into fiat currency (such as euros).

Simply put, there is tax relevance when:

- The investor sells cryptocurrencies for euros

- The holding period was less than 365 days

- Income such as staking or airdrops was received

If you only bought and held the assets throughout the year without selling, there is generally no tax to pay.

What about crypto-to-crypto trades?

Direct exchanges between crypto assets do not, by themselves, trigger immediate tax. The taxable event occurs at the moment of conversion into fiat currency.

Even so, all operations must be recorded with precision. The acquisition date and the price paid will be decisive in the future calculation of capital gains.

Official information and filing instructions can be consulted on the Finance Portal of the Tax and Customs Authority.

How does the 365-day rule work?

The 365-day rule is one of the pillars of crypto taxes in Portugal for 2026. If a crypto asset is held for more than 365 consecutive days before being sold, the capital gain obtained is exempt from taxation. This is a clear incentive for long-term holding.

Practical example

An investor buys 2 ETH in January 2024 and sells them in March 2026. Since the holding period exceeds one year, the gain obtained from the sale is exempt from the 28% tax rate.

However, there are three essential aspects:

- The period is counted separately for each acquired lot

- The exact acquisition date is decisive

- There may be a reporting obligation even in the case of an exemption (Annex G1)

Imagine that part of the coins was bought in February and another part in November of the same year. Each fraction will have its own “tax clock.” One may be exempt; another may still be subject to taxation.

How to calculate capital gains? What is the FIFO method?

The calculation of capital gains for tax purposes on cryptocurrencies in Portugal 2026 must follow the FIFO (First In, First Out) method. This means that the first units acquired are considered the first ones sold.

A simple analogy

Think of an organized line: whoever entered first, leaves first. In tax terms, the oldest purchase is the one that will be used to calculate the gain when a sale occurs.

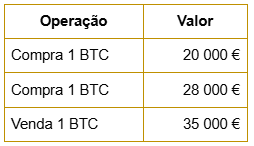

Practical example

To understand how the FIFO method works for crypto taxes in Portugal 2026, see the example below. The goal is to identify which purchase is considered at the time of sale.

According to the FIFO (First In, First Out) method, it is considered that the BTC sold was the first one acquired, that is, the one that cost €20,000.

The taxable capital gain will be: €35,000 – €20,000 = €15,000.

If the sale occurred before 365 days had passed since that first purchase, the autonomous rate of 28% generally applies, unless the taxpayer opts for aggregation.

In a market with strong appreciation, the FIFO method can increase the taxable value, as older acquisitions tend to have lower prices.

Where to report: Annex G or Annex J?

The choice of annex depends on the entity through which the operation was carried out.

Simply put:

- Entity based in Portugal → Annex G

- Foreign entity → Annex J

- Exempt capital gains (>365 days) → Annex G1

The distinction is relevant for the correct reporting framework, even if the applicable rate is identical.

Detailed instructions are available on the Tax and Customs Authority website, including filing manuals and technical clarifications.

A mistake in the annex can delay the processing of the tax return or lead to additional requests for clarification.

How are staking and airdrops taxed?

Crypto taxes in Portugal for 2026 are not limited to capital gains.

Income derived from staking or airdrops is, as a rule, classified as capital income (Category E). Taxation is applied at the autonomous rate of 28%, levied on the value at the time of receipt.

If these assets are subsequently sold with further appreciation, there may be new taxation on the difference between the sale value and the value considered at the date of allocation. This double tax moment requires attention in organizing records and calculating the acquisition value.

Can aggregation reduce the tax?

The 28% autonomous rate applies by default to short-term capital gains. However, the taxpayer may opt for aggregation, integrating the gains into their global income subject to progressive tax rates.

It may be worthwhile when:

- Annual income is low

- The effective tax bracket is lower than 28%

On the other hand, taxpayers in higher brackets will hardly benefit from this option.

Before submitting the tax return, it is prudent to simulate both scenarios to evaluate the real impact.

How to prepare for crypto taxes in Portugal 2026 with greater security?

Effective preparation begins with organization.

The investor should maintain:

- Complete transaction history

- Exact acquisition dates

- Record of commissions paid

- Proof of transfers

The greater the activity, the greater the need for control.

Using a platform that provides a detailed and transparent history facilitates not only risk management but also tax compliance. WEEX provides order history, transaction records, and tracking dashboards so that users can consult and review their transactions in an organized manner, facilitating the control of activities that will need to be considered for tax purposes.

In 2026, the tax filing deadline runs from April 1 to June 30, in accordance with the current tax calendar. Preparing documentation in advance helps avoid errors and delays.

What you should remember about crypto taxes in 2026

Crypto taxes in Portugal for 2026 are based on already established principles: taxation upon conversion to fiat currency, exemption after 365 days of holding, and mandatory application of the FIFO method.

Although the regime is not new, its practical application requires rigor. Dates, acquisition values, and the correct choice of annex are decisive to avoid errors.

Consulting official sources, such as the Tax Authority's Finance Portal, is always recommended to confirm updated instructions.

With proper organization and the use of platforms that provide clear information, such as WEEX, the investor can fulfill their tax obligations with greater predictability, maintaining focus on a sustainable strategy in the crypto market.

Disclaimer

WEEX and its affiliates provide digital asset exchange services, including derivatives trading and margin trading, only where legal and to eligible users. All content provided is for informational purposes only and does not constitute financial advice—seek independent guidance before trading. Cryptocurrency trading involves high risk and may result in total loss. By using WEEX services, the user accepts all associated risks and terms. Never invest more than you can afford to lose. Consult our Terms of Use and the Risk Disclosure for more details.